This three-part series takes an in-depth look at venture capital in India, with the previous part focusing on the India Opportunity from a macroeconomic perspective – you can read the first part here and the the third part here.

The second part of this series explores the state of the Venture Capital Industry and Venture Capital Firms in India and its evolution over time.

Evolution of Venture Capital in India

The phenomenon of Venture Capital (VC) in India is quite young compared to other countries like the US, UK, Europe, or Israel where it has been around for several decades. In the absence of venture capital firms, individual investors and development financial institutions played the role of venture capitalists in India and entrepreneurs largely depended on private placements, public offerings, and lending by financial institutions for funding. It was not until 2010-11 that VC investments began to scale up for real.

The growth of the VC industry in India has followed a sequence of distinct phases:

- Pre 1986: The venture capital industry was in its infancy and adoption of the asset class was done by the central government and government-sponsored institutions only.

- 1986 – 1995: There were a few activities happening within the venture capital space, but it was still restricted to government-sponsored institutions.

- 1995 – 1999: Private venture capitalists from India and abroad started taking interest in the Indian entrepreneurial ecosystem, mainly as a result of successful Indian entrepreneurs in Silicon Valley. In 1993, the Indian Venture Capital Association (IVCA) was established which led to the formalization of the Indian VC community. In 1999, around 80% of total venture capital investments were derived from overseas firms, with 21 venture ccapital firms registered and 8 of them from the public sector.

- 2000 – 2010 (Nascent Stage): VC funds and venture capital firms started testing Indian waters with economic liberalization showing some early positive results and Indian firms becoming more successful in Silicon Valley.

- 2011 – 2014 (Scale-up): This phase saw aggressive VC competition due to an increasing number of deals. LPs view on India’s macro-economic fundamentals was strong.

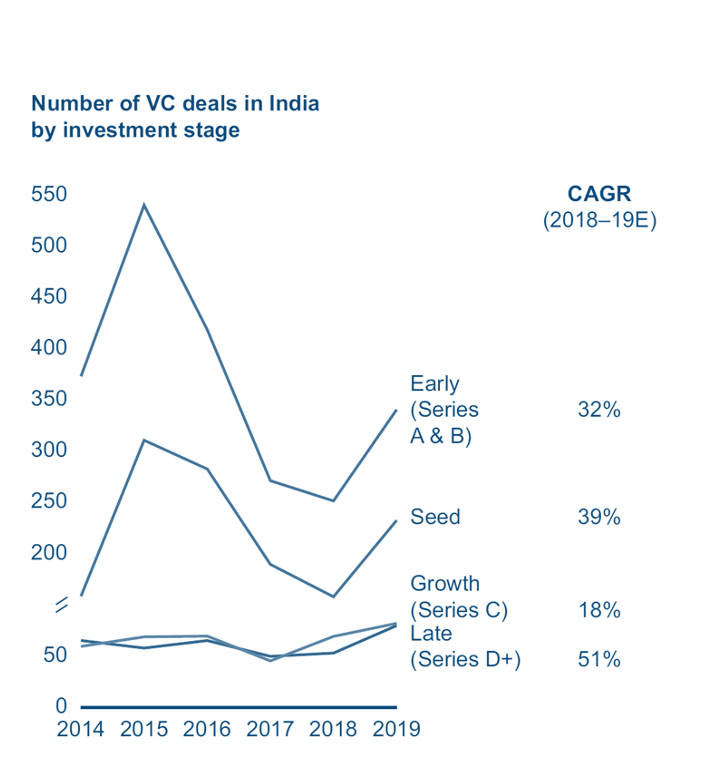

- 2016 onwards (Growth): VCs focused on effecting select deals. As early VC entrants such as Sequoia, SAIF, and Accel evolved, they started focusing on larger deals and this trend is reflected in the broader market.

Venture Capital in India: Updates from recent years

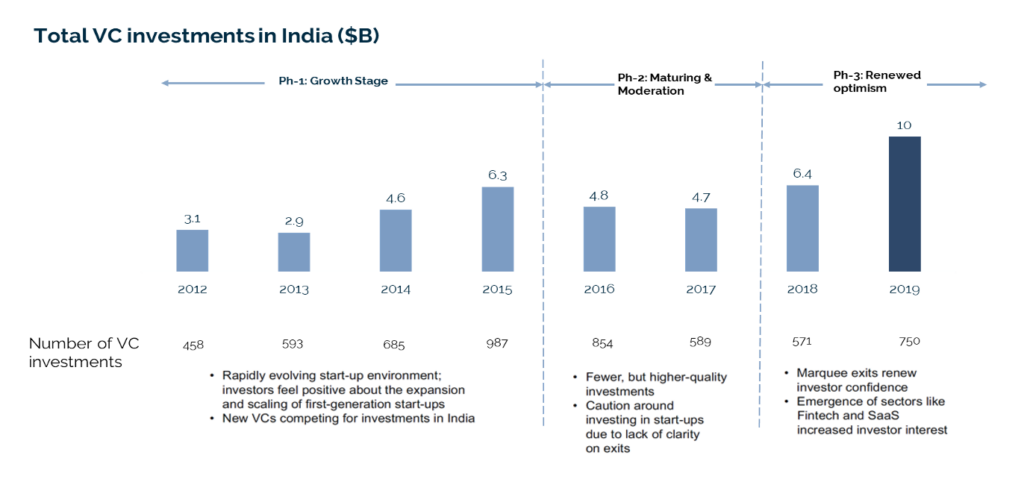

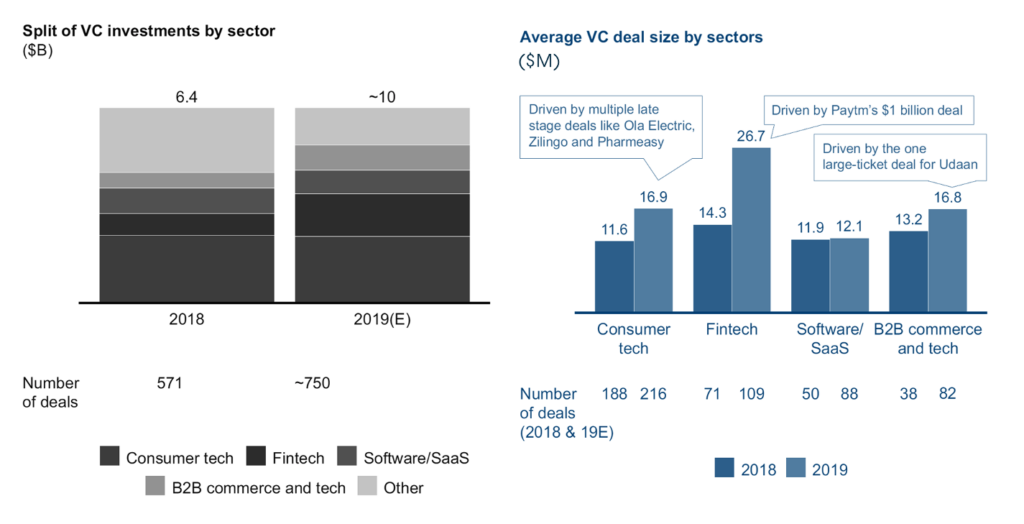

2019 was a milestone year for the Indian VC industry, with $10 billion in venture capital deployed. This was the highest-ever VC investment in India to date and about 55% higher than in 2018.

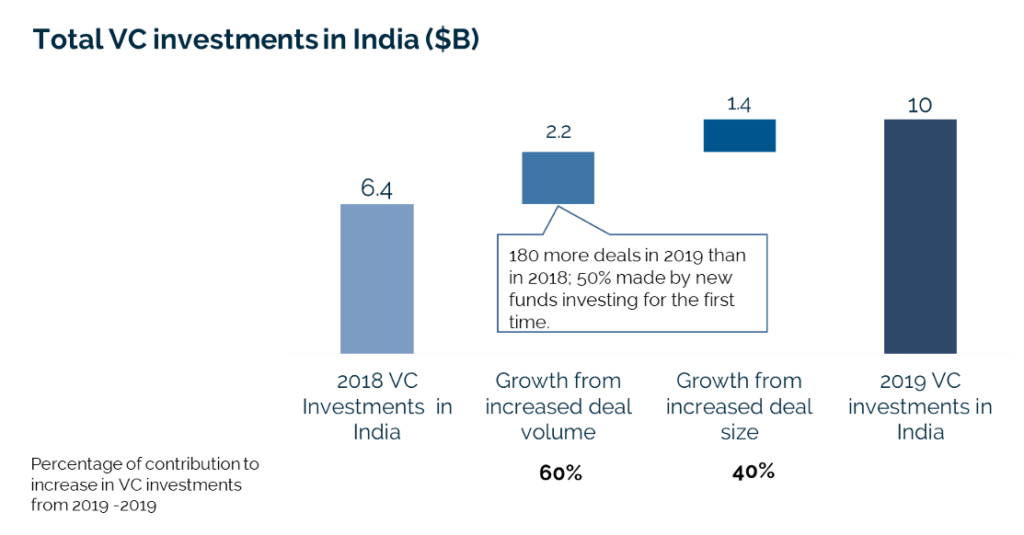

The increased private equity investment in 2019 can be attributed to increased deal volume and increased deal size.

Source: Bain India Venture Capital Report 2020

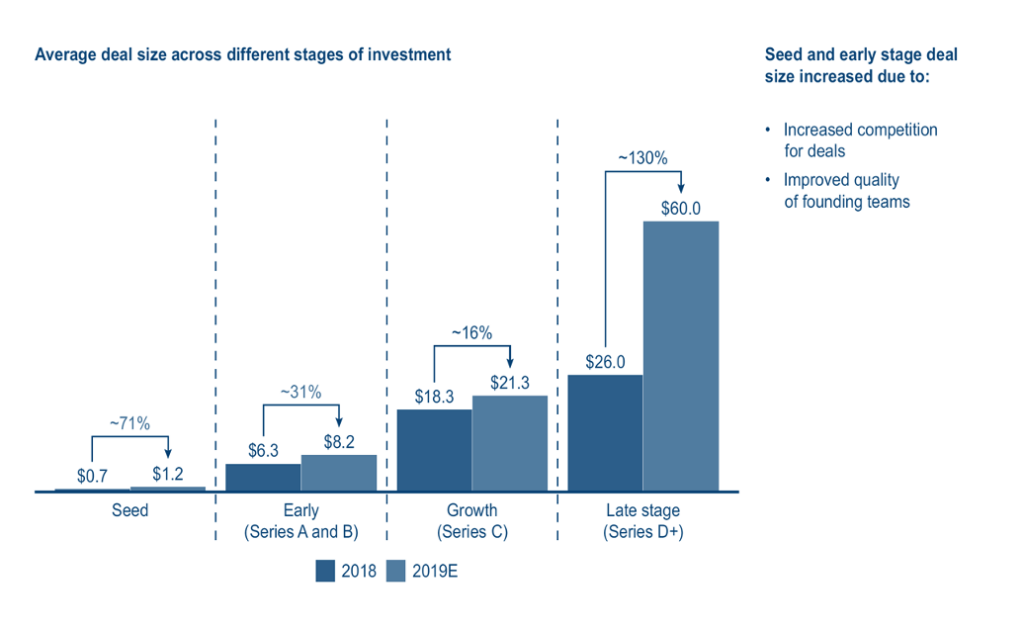

The deal volume in 2019 increased primarily due to more seed and early-stage deals, which accounted for 70% of the deal volume increase. Additionally, the average deal size increased by 20% in 2019 due to the increased share of larger deals.

Despite the large deployment of capital, the dry powder available for VC investing in India was at an all-time high at $7 billion. This is a positive sign for the current year. According to Sidbi State of Sector Report, India had 195 active funds at the end of 2018 (~55% of all registered funds in India), of which 55% have fund sizes less than or equal to US$ 100 million.

In recent years, active funds on average raised 20-25% of their capital from domestic sources, and the remaining from foreign sources. This contrasts with the situation a few years back when the domestic capital pool was generally less than 5%. Key international LPs have been HNIs and large sovereign/ semi-sovereign LPs such as IFC and CDC. Domestic LPs include Indian HNIs, large family offices, and leading institutional investors. Traditional institutional LPs such as pension funds and university endowments are absent in the domestic Indian market.

Additionally, many renowned international venture capital firms have opened their offices in India. Examples include Sequoia Capital India, Saif Partners, Bessemer Venture Partners, Matrix India, IDG Ventures, Accel India, and Lightspeed Ventures.

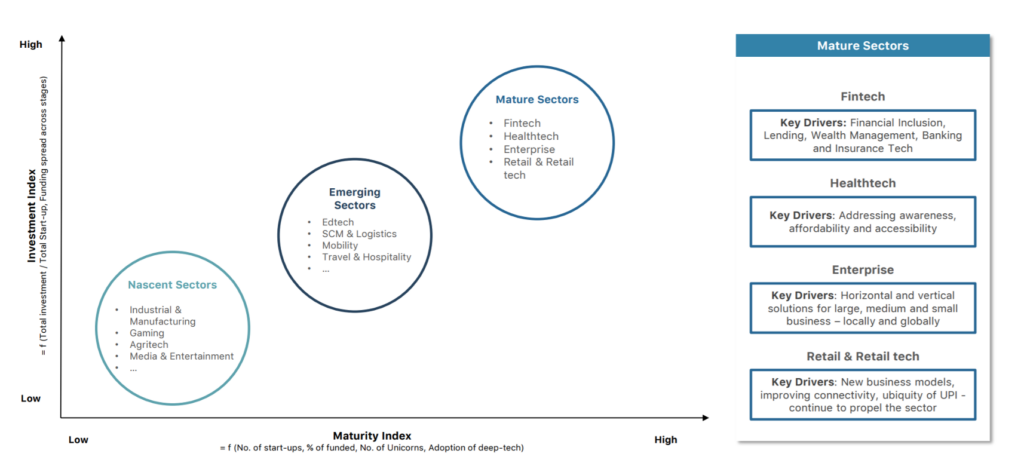

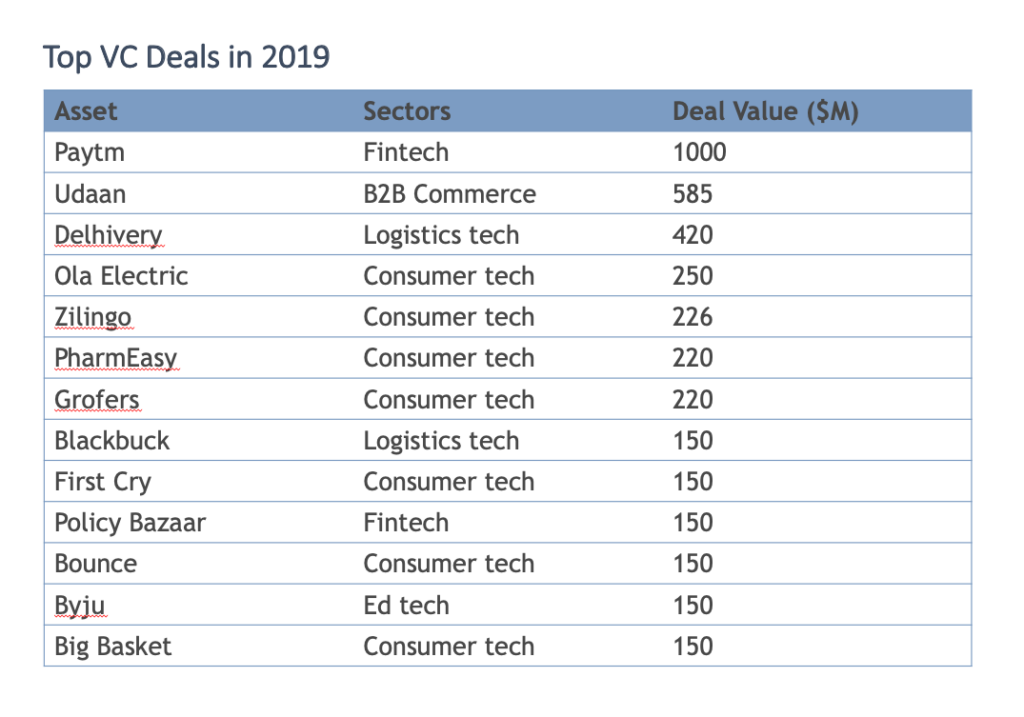

With increasing venture and private equity activities in India, a variety of sectors have emerged at different maturity levels. According to the NASSCOM report on India Tech Start-up Ecosystem 2019, the mature sectors are Fintech, Healthtech, Enterprise Software, and Retail & Retail Tech.

In 2019, 80% of VC funds were invested in four sectors, with the most investment going to consumer tech, followed by fintech, B2B commerce and tech, and Software/SaaS.

The VC Exit Landscape in India

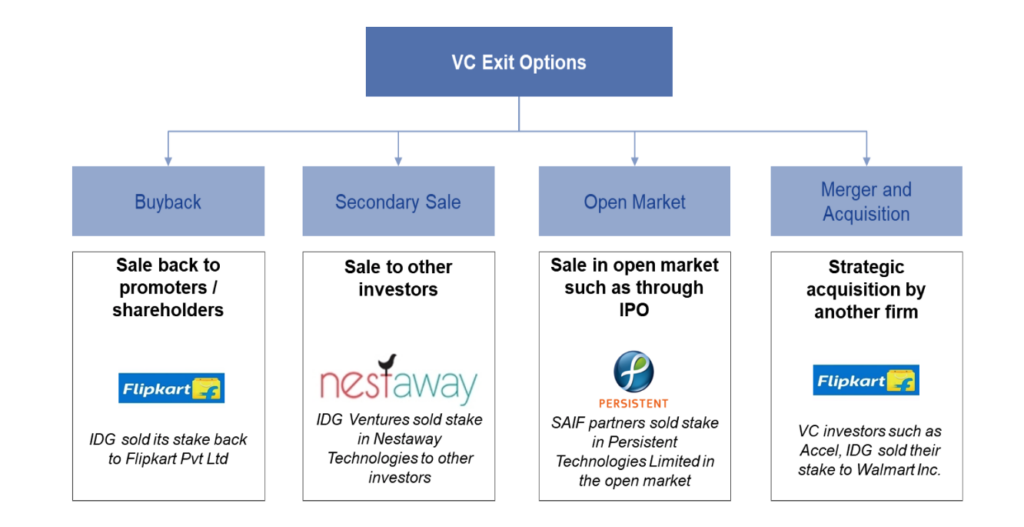

VCs in India mainly exit their investments through buybacks, secondary sales, open markets, or M&A.

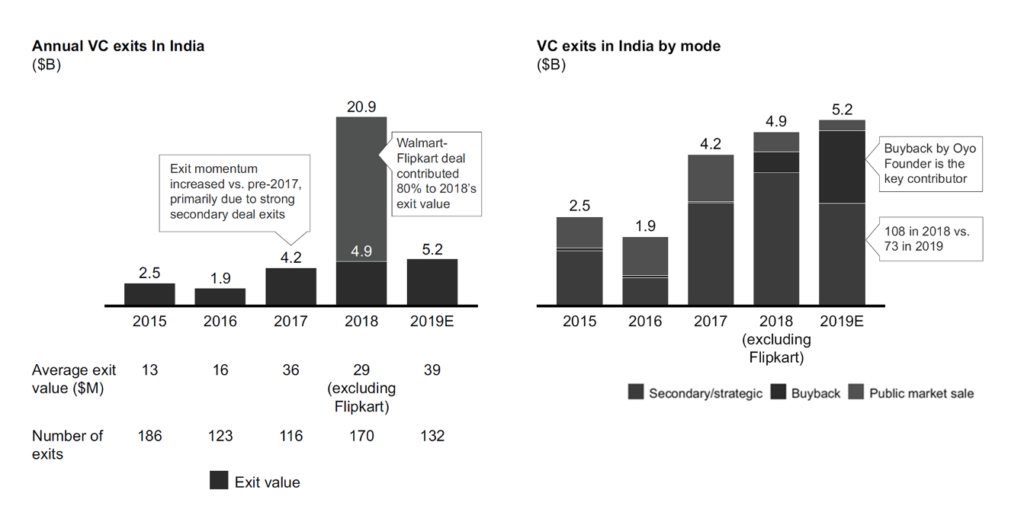

VC exit momentum in 2019 was in line with 2018 (excluding exits from Flipkart sale), with secondary sales leading the mode of exits in India.

2018 saw a marquee exit in the Indian VC ecosystem with the sale of Flipkart to Walmart for US$16 billion.

According to Bain India Venture Capital Report 2020, most of the top funds’ portfolios did not reach maturity in 2019, and exit momentum is expected to increase in the next few years.

The Indian VC ecosystem has come a long way from its modest beginning. The rapidly growing interest among private investors to be part of the growing opportunities and early stage funds in India is a harbinger of better times to come. Marquee exits such as the Flipkart sale to Walmart for US$16 billion have boosted investors’ confidence in the exit landscape of the country. Moreover, most of the top VCs in India have portfolio companies that have not reached maturity thus indicating increasing exit momentum in times to come.

For the VC industry to flourish, there is a need for the startup ecosystem to develop, and that needs to be supplemented by the improving macroeconomics of the nation. Thus, the final part of this series will talk about the state of the startup and early stage fundds ecosystem, the regulatory and structural reforms, and the challenges and risks in the market.

This brings us to the end of part 2 of the three parts series on the Indian Venture Capital Landscape. We hope to engage with you again in the final part of the series.

Here you can find part 1 and here part 3 of the three-part series on the Indian VC landscape.

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the official position of Blue Future Partners.

References:

- Bain – Challenges and opportunities emerge as India becomes third-largest consumer market by 2030

- Bain – India Private Equity Report 2019

- Bain – Perspectives on Indian VC Ecosystem, 2018

- Livemint – 52 startups in India are potential unicorns

- Nasscom – Indian Tech Start-Up Ecosystem

- Preqin – Preqin Markets in Focus: Private Equity & Venture Capital in India, March 2019

- Strategy Business – India ́s New Unicorns

- Venture Intelligence – Venture Intelligence Unicorn Tracker

- White Star Capital – SEA Venture Capital Landscape 2020