What is the economic impact of venture capital in india? Is India an attractive space for venture capital investments? These questions frequent the strategic discussions of many private market investors who want to participate in the developmental journey of the fastest growing trillion-dollar economy in the world.

We at Blue Future Partners were also intrigued by India’s growth and decided to study the country’s potential with respect to the venture capital landscape in India for a time horizon of 10-15 years. In this three-part series, we examine the Venture Capital Landscape and Business Opportunity in India. You can read the second part here and the third part here.

Part 1 – Venture Capital in India: The Macroeconomic View

The first part of the three-part series looks at the Indian Opportunity from a macroeconomic perspective.

The central finding: The macroeconomic indicators for India are strong and healthy, indicating a high growth potential for the Indian economy driven by an upswing in consumption and investments. This positive outlook is driven by three main factors which we will examine in depth below: economic growth, demographics and foreign investments.

1. Economic Growth – India is aspiring to be a US$ 10 trillion economy by 2030

India is the fastest growing trillion-dollar economy in the world, with the annual average GDP growth in the last five years exceeding the growth rate since the start of economic liberalization in 1991. India went from being the 11th largest economy in 2013-14 to the 5th largest economy in 2019, with a nominal GDP of US$ 2.94 trillion (overtaking economies like the UK and France). The country ranks third behind the USA and China when GDP is compared in terms of purchasing power parity at US$ 11.33 trillion.

India’s GDP growth accelerated over 2009-10 due to an upswing in consumption and investments, while its growth over the next five years is estimated to be helped by structural reforms like:

- Policy level initiatives: easing foreign direct investments (FDI) norms and increased limits, credit growth, reduced output gaps

- Active campaigning: Make in India, Digital India, Startup India

- Increased ease of doing business: Introduction of goods and services tax (GST), insolvency and bankruptcy code; and

- Large-scale infrastructure projects: smart cities, industrial corridors, road & rail network.

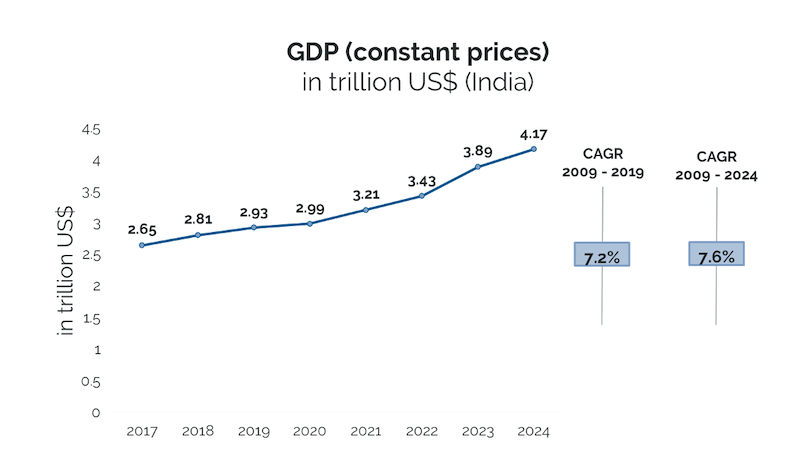

India’s GDP is estimated to reach US$4.7 trillion (INR 330 trillion) by 2024 (US$4.17 trillion adjusting for COVID crisis), with a nominal GDP CAGR of 8.2% over 2019-24. This growth rate is estimated to be ahead of other emerging markets like Brazil (4.7%), China (8%), Indonesia (7.8%) and South Korea (4.8%).

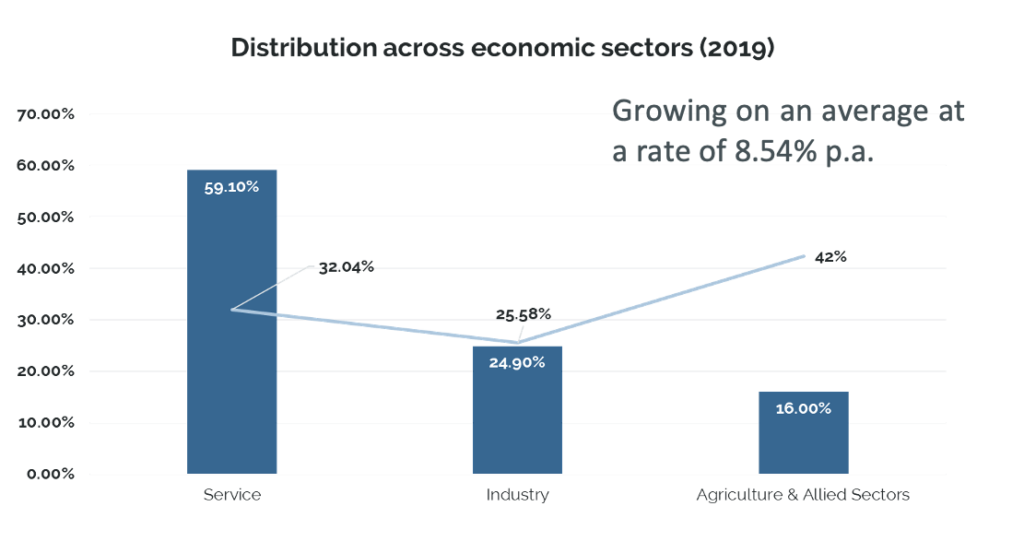

A key driver of strong growth forecasts for India is its diverse economy. Unlike other leading Asian economies, which are export-oriented and heavily focused on manufacturing, India’s growth is propelled by various sectors and an economic base supported by domestic consumption (exports only make up 10% of GDP). The service sector contributes 59% to the total GDP but employs only one third of the population, while the industrial sector contributes 24.9% and agriculture and allied sectors 16%. Agriculture employs 42% of India’s working population. The low exports share is also an upside opportunity for India to further boost its growth.

Moreover, nearly 60% of India’s GDP is driven by domestic private consumption, as compared to 40% in China. Hence, the economy is protected to a great extentagainst external shocks and cycles of low or high public investments.

2. Demographics – India’s attractive demographic profile continues to be a key draw for business

India is the second most populous country in the world and the largest democracy, with 1.39 billion people (2018). There are four key elements that help to understand the strength and evolution of demographic diversity in India.

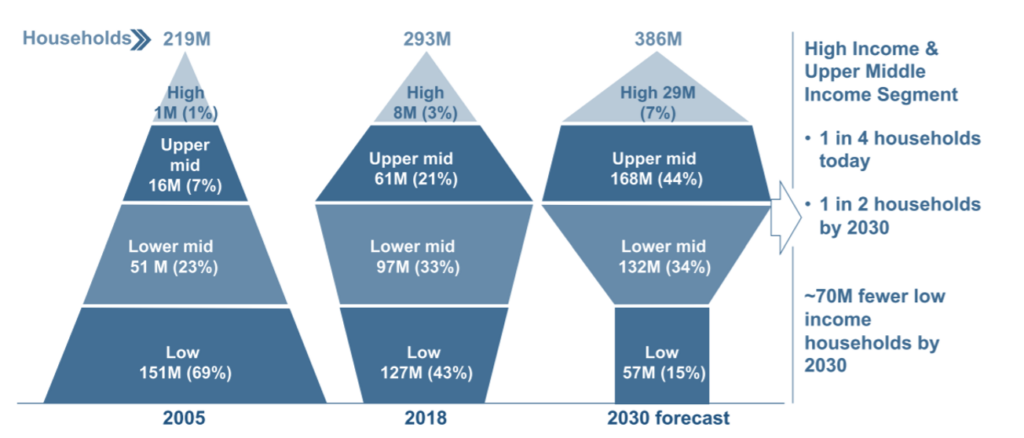

a. Evolution of household-income profile in India

The middle-income class and high-income class segments will see a significant expansion until and beyond 2030. As shown in the chart above, in 2018, the upper-middle class and high class is made up of 24% of the total households and these numbers will expand to 51% of total households by 2030.

The upper middle-income households will drive 47% (US$2.8 trillion) of total consumption, and high-income households will drive another 14% (US$ 0.8 trillion) by 2030 as compared to 30% and 7% respectively in 2018.

Moreover, India will lift nearly 25 million households out of poverty by 2030 which would imply that less than 5% of households will lie below the poverty line by 2030, down from 15% in 2018.

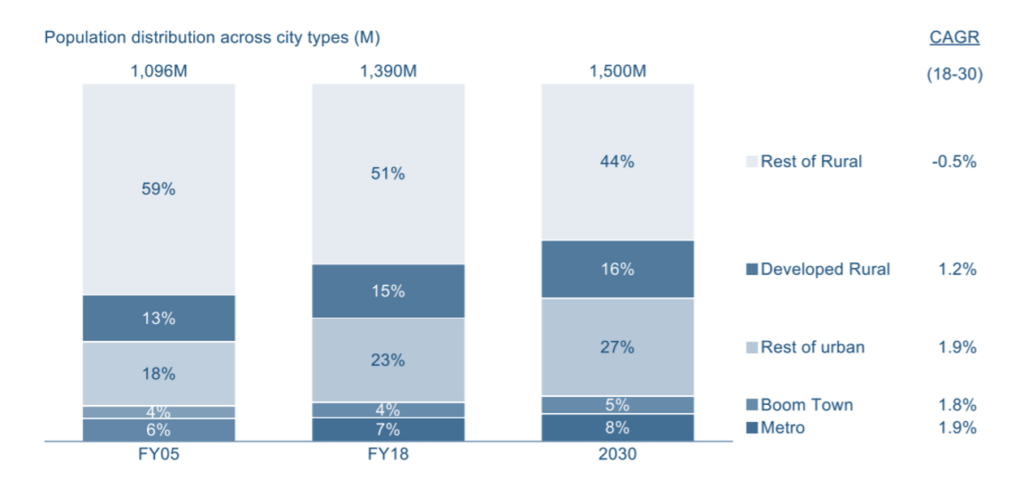

b. Steady and dispersed urbanization

By 2030, 40% of Indians will be urban residents as compared to 34% in 2018. The rural per capita consumption will grow 4.3 times by 2030, compared to 3.5 times in urban India (all comparison to 2018 figures). With incomes in developed rural towns already mimicking those in small towns and greater internet penetration narrowing digital divides, the erstwhile urban-rural paradigm may no longer be the most accurate lens to assess aspirations and preferences across India.

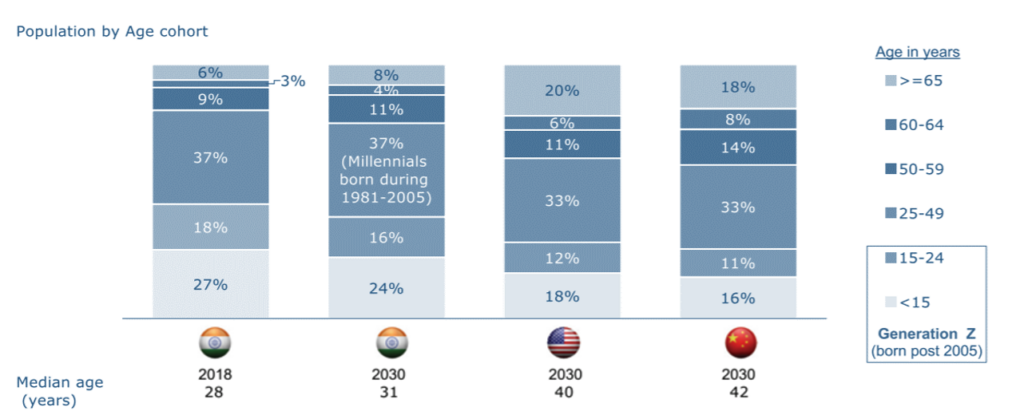

c. In 2030, 77% of India’s population will be Millennials and Gen Z

Working- age majority: With a median age of 31 in 2030 (versus 42 in China and 40 in the US), India will remain one of the youngest nations in the world with one of the largest working-age populations. India will add more working-age citizens to the world than any other country in the next decade.

Young millennial households: By 2030, India will add nearly 90 million new households headed by millennials who were born into a liberalized India. Having grown up with better education and employment opportunities and having higher incomes, they will likely break away from the frugal attitudes of their preceding generations.

Rise of digital natives: In 2030, India will have about 370 million Generation Z consumers of ages 10- 25, who will have grown up in an India with ubiquitous internet, smartphones, digital media and digital platforms. As they start earning and spending, they will actively use technology enabled consumption models and in turn influence consumption behaviour of their household.

d. Technology and Innovation

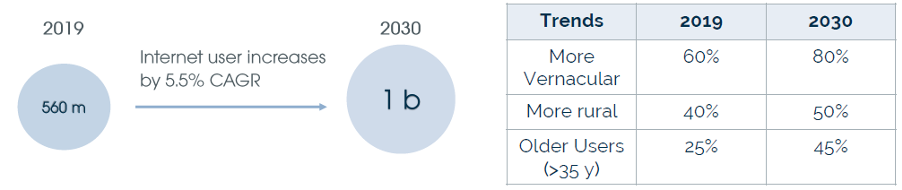

India is experiencing a third wave of telecom revolution led by voice-based user interaction, vernacular and video content. By 2030, the country will have 1 billion diverse internet users, with more vernacular, rural and older users.

At the same time, India is a mobile- first market, with a significantly higher mobile market share than other countries. Whereas around 80% of Indians access the internet via mobile devices, mobile penetration in the US is at 51% and 58% in China, creating a different profile of connected consumers for businesses to target.

3. Foreign Investment – India is becoming increasingly attractive to foreign investors

The improving macroeconomic environment over the last decade has supported economic growth. Inflation remains under the target of 5% (2019: 4.54% & 2020: 3.34% ), the current account deficit has been reducing (reduced till 2017 to 0.6% of GDP, increased in 2019 to 2.1% of GDP but falling oil prices are expected to keep this low), foreign exchange reserves continue to swell (reached US$ 424.5 billion in 2018, decreased in 2019 to US$412.9 billion) and the Indian currency continues to show sign of stability in comparison with other closely competing emerging economies.

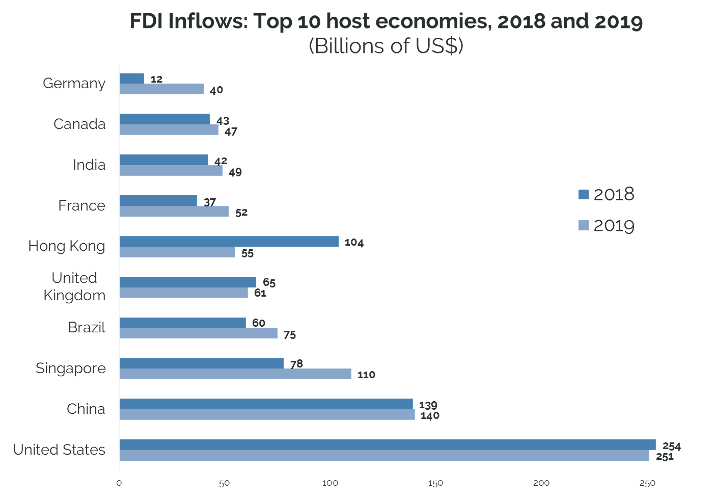

These factors have been contributing to improving FDI (Foreign Direct Investment) inflows. India has witnessed improvement in the investment scenario with investments across various sectors of the economy. India ranked 8th in FDI inflows with US$ 49 billion worth of inflows in 2019.

Some recent FDI in India include:

- In June 2020, Jio Platforms sold a 22.38% stake worth US$ 14.75 billion to Facebook, Silver Lake, Vista, General Atlantic, Mubadala, Abu Dhabi Investment Authority, TPG, and L. Catterton. This is the largest continuous fundraise by any company in the world.

- In January 2020, Amazon India announced an investment of US$ 1 billion for digitizing small and medium businesses and creating one million jobs by 2025.

- In August 2019, Reliance Industries (RIL) announced one of India’s biggest FDI deals with Saudi Aramco to buy a 20 per cent stake in Reliance’s oil-to-chemicals (OTC) business at an enterprise value of US$ 75 billion.

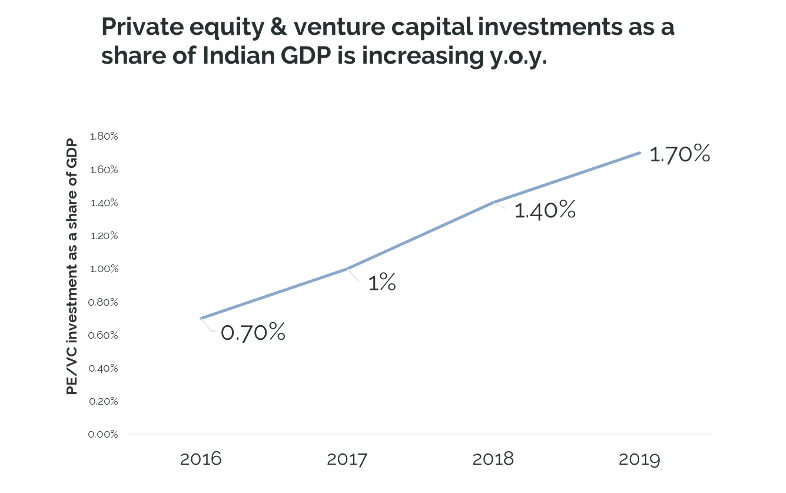

The private equity and venture capital investments as a share of Indian GDP is increasing year over year and as of 2019, it was at 1.7% of GDP. Here, private equity includes buyouts, private investing in public equity, expansion, turnaround, mezzanine -IPO, and bridge loans.

In 2018, the PE to VC investments ratio in India were at 3.2x, which is higher when compared to China (0.9x), Indonesia (1.5x) and South Korea (2x).

Compared to private equity, the venture capital ecosystem in India has had a late start. Though theoretically the financing of early stage companies commenced during the technology boom in the late 1900s, it was not until 2010-11 that VC investments began to scale up.

This brings us to the end of part 1 of the 3 parts series on the Indian Venture Capital Landscape. The next part of the series will talk about the state of Venture Capital industry in India and its evolution.

Here you can find part 2 and here part 3 of the three-part series on the Indian VC landscape.

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the official position of Blue Future Partners.

References:

- Bain – Challenges and opportunities emerge as India becomes third-largest consumer market by 2030

- Bain – India Private Equity Report 2019

- Bain – Perspectives on Indian VC Ecosystem, 2018

- Livemint – 52 startups in India are potential unicorns

- Nasscom – Indian Tech Start-Up Ecosystem

- Preqin – Preqin Markets in Focus: Private Equity & Venture Capital in India, March 2019

- Strategy Business – India ́s New Unicorns

- Venture Intelligence – Venture Intelligence Unicorn Tracker

- White Star Capital – SEA Venture Capital Landscape 2020