Entering the second decade of the 21st century, quantitative easing and technology monopolies have reached unprecedented heights. Among institutional limited partners and family offices (‘LPs’), the growing interest in alternative asset class allocation is unmistakable. Climbing towards the top of the LP’s agenda are challenger VCs, early stage venture capital (‘early stage VC’).

While keeping an eye on the early stage VC stalwarts, we also closely track the fringes of the industry.

Here, we are seeing a new cohort of managers eagerly wading into this void, armed with contrarian investment philosophies and strategies looking fairly different, if not entirely at odds, with your household names of early VC.

Here, we are seeing a new cohort of managers eagerly wading into this void, armed with contrarian investment philosophies and strategies looking fairly different, if not entirely at odds, with your household names of early VC.

Our research takes a first principles approach to discuss the rise of challenger VCs and how they may fulfil the risk return profiles sought by LPs. Specifically, we ask ourselves:

· What are challenger VCs?

· How do the economics work for challenger VCs?

· How do we due diligence challenger VCs?

· How should LPs compare challenger VCs vs traditional VCs?

· What does the future hold for early stage VC?

—

Spotting challenger VCs

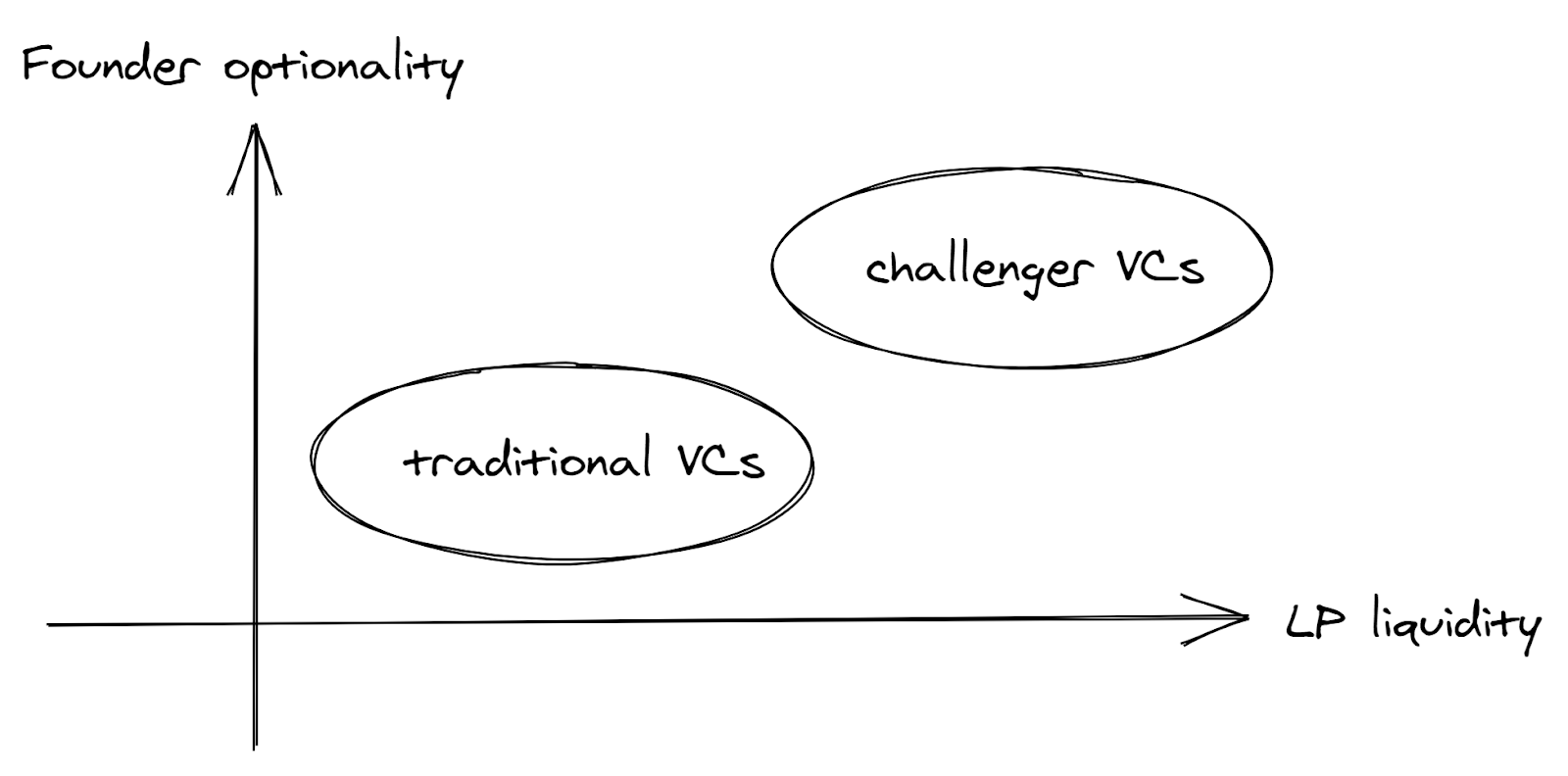

We note that challenger VCs usually differentiate from traditional VCs in two ways.

LPs can expect sooner distributions from challenger VCs, instead of decade-long lock-ups prevalent in early stage VC whilst delivering the typical return multiple as expected.

(How this is done is best illustrated through a sample portfolio construction walkthrough, which we cover in detail below.)

Challenger VCs are also attracting a new class of successful founders running capital efficient businesses whose upside LPs have yet to be able to access. Armed with sustainably high growth, if not already profitable businesses, founders prefer less restrictive forms of funding given the increasingly well publicised drawbacks of venture.

Whether the slogan of ‘greater founder optionality’ can gather a stable of high growth companies that bears out the challenger VC thesis is yet to be seen. However, our deep dive into the challenger VC fund economics shows signs of promise.

The Economics of Challenger VCs

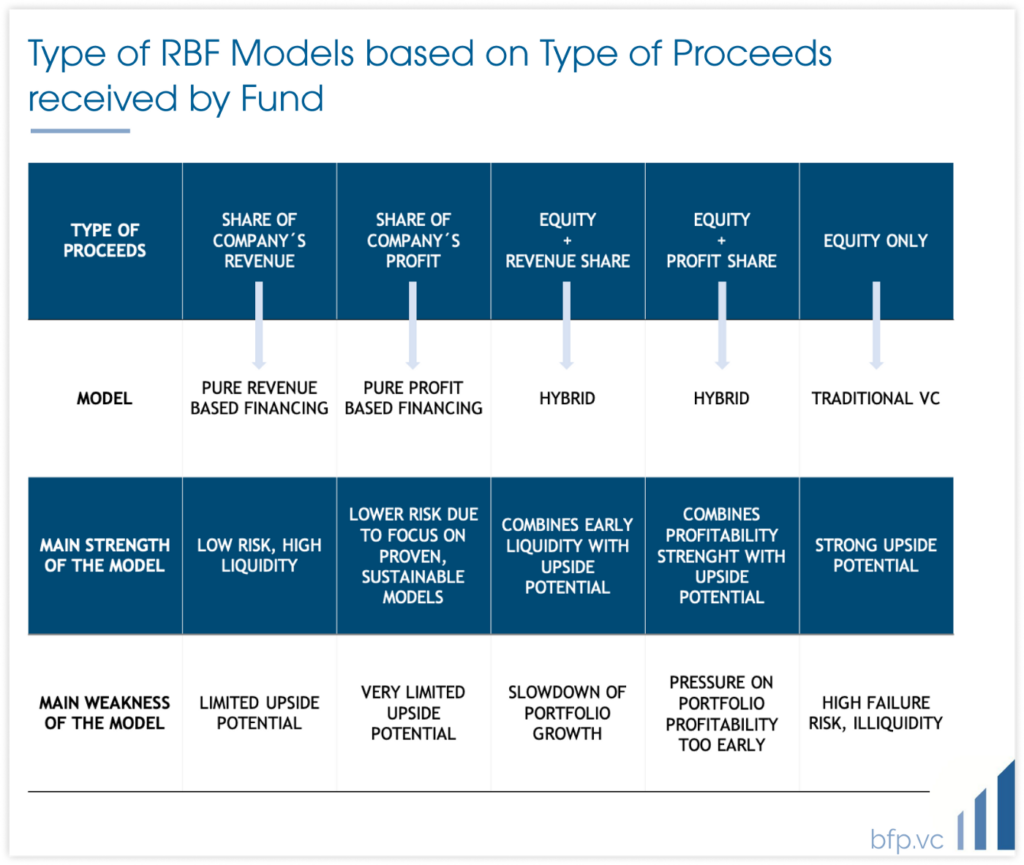

Generally, from the perspective of challenger VCs, proceeds can be obtained from a combination of two components:

1. Equity (sale or IPO)

2. Revenue (or Profit) sharing (which we call the Liquidity Component)

Proceeds consisting purely of the first is no different from traditional VC. Proceeds consisting purely or partially of the second is what distinguishes challenger VCs.

After investing, the fund will receive over a certain period of time (usually few years) a share of the Revenues (or the Profits) up to a limit (a cap), which is usually around 2–4x.

For instance, if the fund invests US100k with a 4x cap, the company will repay its Revenues (or Profits) to the fund over time until a cumulative amount of US400k is reached.

The precise design mechanism of the economics depends on the specific fund model. One aspect we noticed in our research is that there is no standard framework and each firm has its own.

For instance, the Equity component is integral to some models, but missing in others. For certain challenger VCs, the Liquidity component is generated from Revenues, while others from Profit sharing.

The different types of models in the market are summarized in the chart below together with their main strength and weakness:

The Due Diligence for Challenger VCs

Each model poses different questions and it is quite difficult to generalize, but, taking the hybrid models as an example, we believe there are several crucial aspects to understand when diligencing the economics of RBF funds.

1. Are the returns coming mostly from the Equity or Liquidity component? Does the Liquidity component return at least entirely the capital, and in what time frame?

The composition of the total expected return is a key aspect of how challenger VCs succeed. In hybrid models, these two return components serve different functions:

· The Liquidity component serves as a mechanism of risk reduction by providing early liquidity. Basically, the more total returns are dependent on repayments, the less the downside risk.

· The Equity component provides the model with upside potential or additional residual value after the Revenue Share.

The dependency of the model on equity proceeds is fundamental to understand because challenger VCs are targeting companies with a different risk profile than traditional VC.

The more the model is dependent on equity, the more the fund is similar to a traditional VC, and the more its risk profile will be similar to a normal VC fund.

2. Can you elaborate on key assumptions behind return expectations of the Liquidity Component alone? What are key assumptions behind revenue or profit repayments?

This aspect is especially relevant for Profit sharing models.

Let’s take an example: a challenger VC invests $250k in a company that has to return 2.5x such amount with a profit share of 20% in 4 years.

This means that the company has to give back to the investor a total amount of $625k ($250×2.5x), which means $156k per year ($625/4).

It follows that the company has to produce yearly profits of $780k ($156/20%). If the company has a 10% profit margin, then the yearly revenues necessary for the model to work are $7.8m ($780/10%).

A company that needs $250k of financing today (equivalent of a pre-Seed round at pre-Revenue stage) needs to grow in 4 years to $8m in Revenues. This is fairly ambitious and impractical (almost comparable to a Series B — Series C profile), especially when challenger VCs should be targeting less risky and therefore less high startups. Hence a word of caution:

Always assess the underlying financial targets that portfolio companies are expected to hit. Sometimes, it exposes unrealistic growth expectations that are antithetical to fundamental ways challenger VCs seek to differentiate in the first place.

3. How about from the Equity component alone? How does this compare with traditional VC benchmarks?

Comparison with traditional VC benchmarks is interesting if a challenger VC depends heavily on the Equity component to make up its total returns.

Generally, we find that challenger VCs aim to construct portfolios that do not follow power law distributions, which expand the universe of potential investments and lowers the overall risk profile.

4. What are other key portfolio construction assumptions underlying your strategy?

This is where challenger VC and traditional VC due diligence converges. Deployment pace, entry valuations, and return expectations, among others, are important to consider.

As an exercise for our readers, we created a very simple model on Google Sheets that readers can download to test assumptions by inserting inputs in the yellow cells.

The model is just a simplified example, does not cover important aspects of the economics of RBF funds and it is not suitable for assessment, evaluation, or analysis, but only for learning purposes.

Comparing Challenger VCs with Traditional VCs

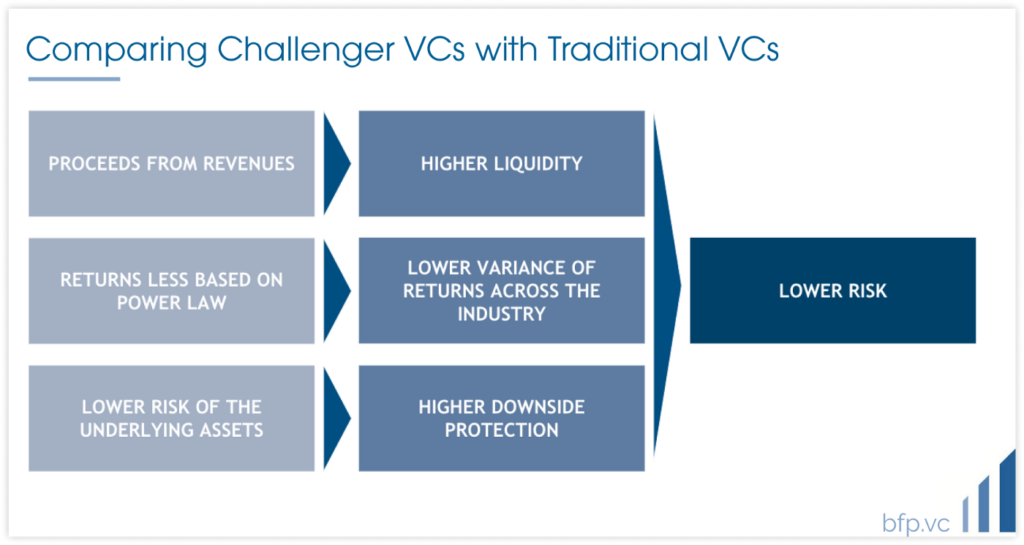

Challenger VCs offer a lower risk product for potential LPs to enter early stage VC, due to three main elements:

1. Faster Liquidity. From an LP perspective, an investment in traditional VC funds poses great problems of long term liquidity planning. Challenger VCs receive cash from their portfolio, which can be distributed early. Moreover, earlier liquidity also implies a better performance at IRR level, if compared to a traditional VC reaching the same money multiple but with later liquidity.

2. Diversification from power law. Traditional VCs usually need to invest in the top 1% of the companies to achieve meaningful returns. Given that only 1% of the VCs manage to do that, VC returns partly follow power law as well (only few VCs are successful, most are not). This leads to a high variance in VC performance (higher than other asset classes), which is of course a risk. In contrast, challenger VCs do not necessarily target rocket ships and hence return variance should be theoretically be lower than traditional VC.

3. Exposure to the camels and zebras of early stage VC. The focus on “sustainable”, capital efficient, and downturn resilient playbooks makes the underlying assets of challenger VCs less risky, which consequently provides a new angle of downside protection for LPs.

The biggest question is this: Is it the right time to invest in challenger VCs? Or is it still too early?

Here are three hurdles for potential LPs to begin their manager selection journey:

1. Lack of track record. In practice, challenger VCs still number few and far between, and no successful track record has been widely publicised to put traditional VCs on notice. It is still a relatively unproven concept with no key leaders to back.

2. Deal sourcing and access. Without a track record to point to, will challenger VCs actually be able to secure allocation in the unconventional profile of cashflow positive, EBITDA positive, or otherwise perfectly self sustaining startups?

3. Manager value add. Suppose challenger VCs do secure a spot. While eschewing the path to become a unicorn creates more options, challenger VCs still have their work cut out for them to groom their portfolios and grow from 100k in Revenues to 500k or 1m without resorting to blitzscaling and other capital-inefficient means.

Future of Challenger VCs

The early stage VC space will be interesting to monitor with the arrival of challenger VCs. It will likely become bigger and more dynamic in the future.

We expect the number of challenger VCs to increase from now on. We also expect increasing competition due to a set of new incumbents with similar models and offerings, ranging from banks to startups.

Over time, successful transactions and knowledge spillover may also lead to a greater standardization of the models towards similar economic mechanisms and investment frameworks.

Don’t be surprised to find even traditional VCs getting in on the act. Investing in challenger VCs, carving out allocations for startups that used to only interest challenger VCs, or launching new vehicles with a challenger VC model under their established brand are all within the realm of possibility.

To potential LPs, the big question is whether to enter the market early to secure an allocation in the top funds or to wait until more information is available and the market matures as brands establish themselves.

Meanwhile, start grilling existing managers how they plan to solve for faster LP liquidity and greater founder optionality. At the first sign of dithering, make them read this article!

—

Authors: Hampton Tao (New Heritage) and Marco Cesare Solinas (Blue Future Partners)

About Hampton Tao

Hampton serves as Assistant Manager of Special Projects at New Heritage Group and C.F. & Nancy Tao Foundation. He is passionate about investment, philanthropy, and emerging models of doing good at scale.

Hampton holds a Bachelor’s and Master’s Degree in Manufacturing Engineering from the University of Cambridge.

Linkedin — Twitter — Substack

About Marco Cesare Solinas

Marco is an Analyst at Blue Future Partners, where he is responsible for sourcing and analyzing new investment opportunities. He is passionate about Technology, Venture Capital and making an impact with investments.

Previously, he has built an international and multicultural background across Italy, US, Germany, Turkey, and Malaysia.

Marco holds a CEMS Master’s in International Management and a Bachelor in Economics and Finance from Bocconi University.

Linkedin — Twitter — Medium

About New Heritage

New Heritage (http://www.nh-holdings.com) is a single family office with a background in real estate. Our investment activities began in 2014 after we sold our controlling interest in a real estate company we listed on the Hong Kong Stock Exchange since 2005. Currently we are active LPs looking at early stage venture and impact investment.

About Blue Future Partners

Blue Future Partners (www.bfp.vc) is a Fund of Funds with decades worth of experience in investing in Venture Capital. We specialize in backing emerging managers focused on early stage technology investments. We are people-centric and relationship-driven. We have a global mandate and existing relationships with Emerging Managers in the US, Europe, Israel, China and South East Asia.